Do You Have a Mortgage Plan?

You Should Review Your Mortgage Plan Soon. Here’s Why.

You have a financial plan.

Maybe an estate plan.

Possibly life insurance, too.

But do you have a mortgage plan?

Most people set up their mortgage and never think about it again. But a mortgage is a long-term part of your financial life. It deserves regular attention.

Think about it. You revisit your finances and insurance when things change. Your mortgage should get the same review.

Here are three opportunities to review your mortgage plan:

1. Life Events

Marriage, growing your family, divorce, or preparing for retirement often change your financial priorities. Your mortgage should reflect that.

2. Changes in Income

A new job, raise, job loss, or side income can impact your ability to borrow or pay off your mortgage more effectively.

3. Regular Check-Ins

Even if nothing big has changed, reviewing your mortgage every year helps you stay on track and spot new opportunities. For example, one of my clients may discover she has enough equity to drop her mortgage insurance, which could save her nearly $200 a month. Another might realize her adjustable-rate mortgage is about to reset. A mortgage plan review would give her time to refinance before her payment increased.

These check-ins are quick and easy, and they can make a big difference over time.

What does your mortgage plan review involve?

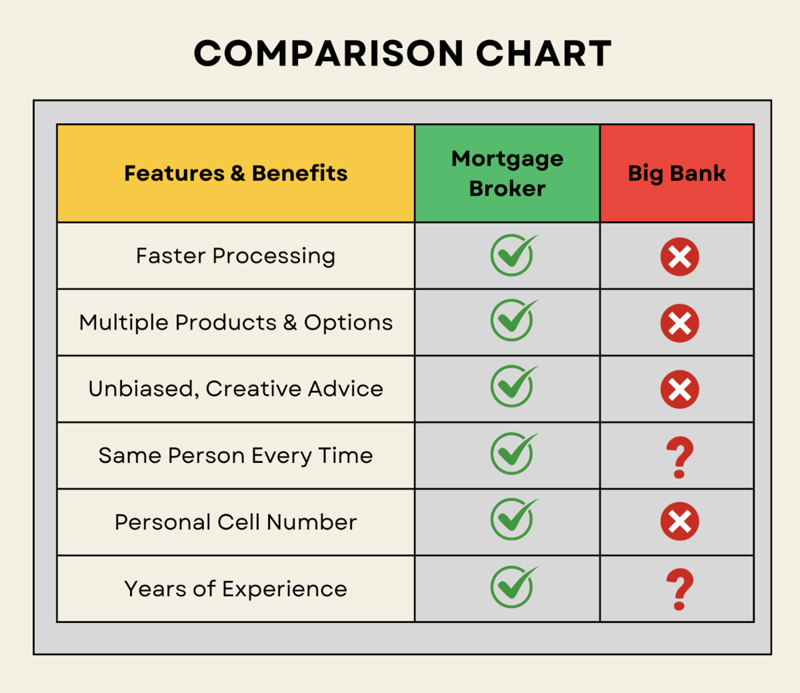

- Rate Check: Could you get a better interest rate?

- Equity Check: Has your home gained value, and could that equity serve another purpose?

- Product Check: Is your current mortgage still aligned with your goals?

Your mortgage needs to work for your future, not just your past.

Let’s set up a quick review. I’ll walk you through it and help you make sure your mortgage is still the right fit.

* * * * *

Ready to buy a new home or refinance the one you own? Please get in touch and I’ll be happy to answer your questions and help guide you through the process. I look forward to speaking with you.

Summer Solstice

It may not feel like summer yet with cool weather and more rainy days than anyone needs. Nevertheless, the summer solstice, arriving this year on June 20, is the official kickoff of summer.

Solstice has been celebrated for thousands of years across nearly every culture. It marks the longest day of the year, when the sun reaches its highest point in the sky and daylight stretches to its fullest.

Ancient civilizations treated the solstice with great respect. In England, Stonehenge was likely aligned with the rising sun on the solstice, and people still gather there each year to welcome the light. In Scandinavia, Midsummer festivals with bonfires and maypoles are still popular.

The ancient Egyptians even timed the construction of their pyramids around the sun’s position at solstice.

It’s a time to pause, enjoy the extra daylight, and reconnect with the natural rhythms that have guided people for millennia. Happy summer!

Home Improver: Why Do My Squished Ants Smell Funny?

As you know from reading this section, from time to time we turn to science to better understand our homes. More important, we don’t shy away from the burning questions that keep homeowners like you up at night.

So let’s dive into the reason why some ants smell when you squish ’em.

If you’ve ever squashed a tiny intruder and caught a whiff of lemony furniture polish or Windex, congratulations — you’ve likely met (and murdered) the citronella ant. These ants can be pale yellow and release a citrusy odor when crushed, which is a natural defense mechanism. In ant terms, it’s basically, “You may have won the war, but you’ll never forget me.”

Despite the fancy fragrance, citronella ants are pretty harmless. They don’t sting, bite, or raid your pantry. They mostly just hang out underground, but some drop by to say hello if water is pooling anywhere in your home. Even a small amount of water collecting on a windowsill will attract them.

Now, before you go around sniffing every ant in your kitchen, know that not all odorous ants are created equal. Enter the odorous house ant: same idea, way worse smell. Think rotten coconut instead of lemon zest. Definitely not a candle scent you’ll see at HomeGoods.

So next time you notice a weird smell after a squish, you’re not losing your mind, you’re just experiencing one of nature’s weirder party tricks.

The more you know!

Many homeowners set up their policy at closing and never revisit it. The problem? A lot can change in just a few years. The cost to rebuild your home may have gone up. You might have made improvements like finishing a basement, updating a kitchen or adding solar panels. Or maybe you’ve acquired higher-value personal items like jewelry, artwork or electronics. If your policy hasn’t been updated to reflect these changes, you could be underinsured. That could lead to financial stress in the aftermath of unfortunate events.

Many homeowners set up their policy at closing and never revisit it. The problem? A lot can change in just a few years. The cost to rebuild your home may have gone up. You might have made improvements like finishing a basement, updating a kitchen or adding solar panels. Or maybe you’ve acquired higher-value personal items like jewelry, artwork or electronics. If your policy hasn’t been updated to reflect these changes, you could be underinsured. That could lead to financial stress in the aftermath of unfortunate events. Once the danger of frost has passed, usually after Mother’s Day, you can transplant your tomatoes outdoors. Choose a spot with full sun and well-drained soil, and don’t forget to

Once the danger of frost has passed, usually after Mother’s Day, you can transplant your tomatoes outdoors. Choose a spot with full sun and well-drained soil, and don’t forget to  Deodorize and Freshen Spaces: Sprinkle baking soda in your fridge, trash cans, or shoes to neutralize odors. Its odor-absorbing power works wonders in keeping spaces smelling fresh without artificial scents.

Deodorize and Freshen Spaces: Sprinkle baking soda in your fridge, trash cans, or shoes to neutralize odors. Its odor-absorbing power works wonders in keeping spaces smelling fresh without artificial scents. What to Look For in Dog-Safe Ice Melt

What to Look For in Dog-Safe Ice Melt Weather Stripping: Apply adhesive weather-stripping tape around door and window frames. This simple solution seals gaps and stops drafts, making your home more energy-efficient.

Weather Stripping: Apply adhesive weather-stripping tape around door and window frames. This simple solution seals gaps and stops drafts, making your home more energy-efficient. 1. Install Gutter Guards

1. Install Gutter Guards

Marigolds are typically the go-to for many gardeners. Their strong scent is off-putting to rabbits, and they add a splash of color to any garden. Lavender may give off a soothing aroma to humans, but for rabbits its potency acts as a repellent. Another option is the snapdragon; its bitter taste and tall, thick stalk makes them less appealing to your furry interlopers.

Marigolds are typically the go-to for many gardeners. Their strong scent is off-putting to rabbits, and they add a splash of color to any garden. Lavender may give off a soothing aroma to humans, but for rabbits its potency acts as a repellent. Another option is the snapdragon; its bitter taste and tall, thick stalk makes them less appealing to your furry interlopers.